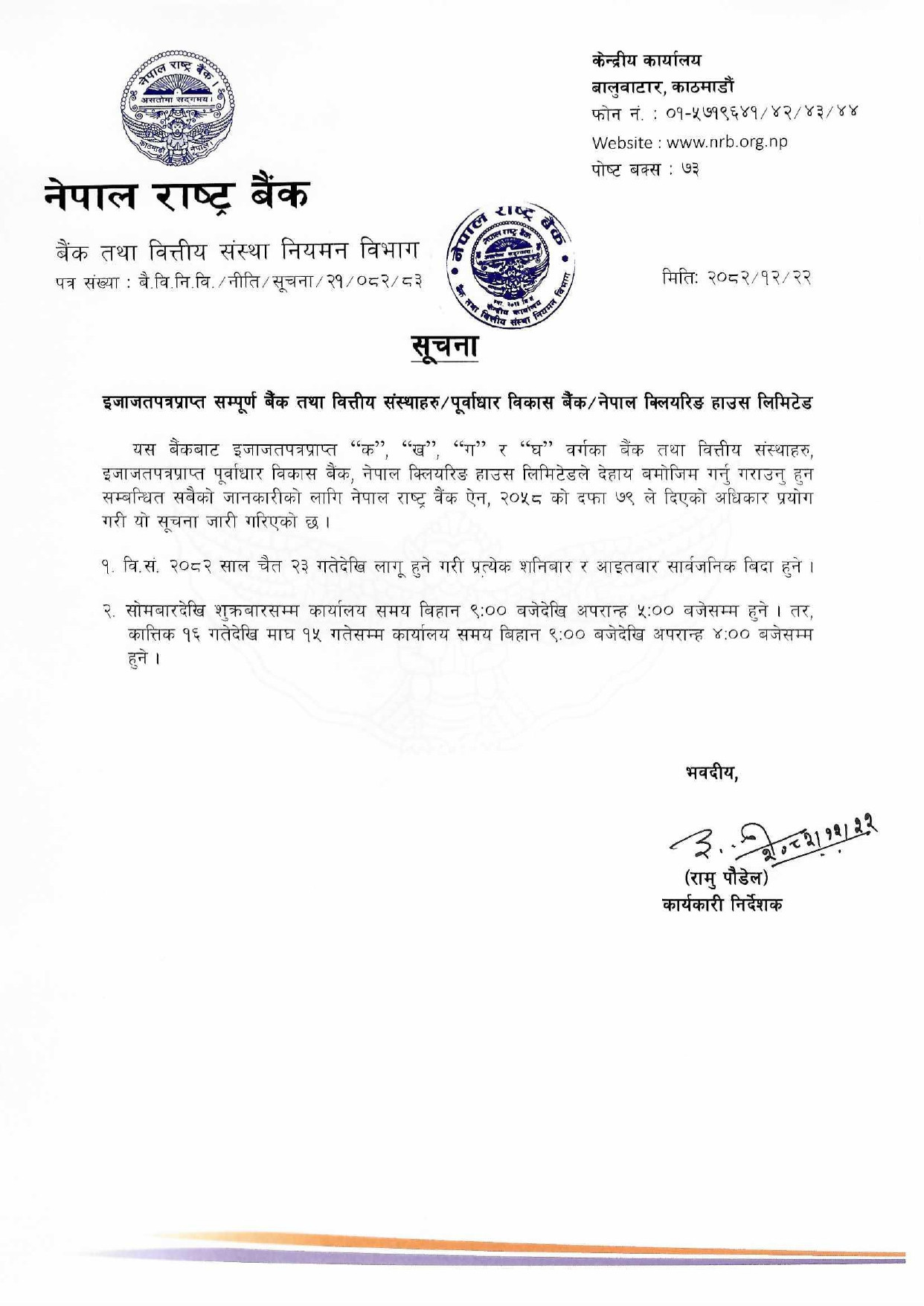

Kathmandu. Nepal Rastra Bank quarterly review of monetary policy. Confederation of Banks and Financial Institutions Nepal (CIBIFIN) has given various suggestions for the review of monetary policy.

These are CBFIN's recommendations

1. The provisions of the Bank and Financial Institutions Act (BAFIA) which gradually converts the founder shares into ordinary shares should be implemented. It seems that the implementation of such a system will directly help in building and operating sufficient capital. In addition to keeping uniformity in the market price of founder shares and common shares, in the case of founder share loans, such as ordinary share loans, the average price of the last 180 working days published by Nepal Stock Exchange Limited or the prevailing market price of the shares, whichever is lower, shares only up to 70 percent of the value. A provision should be made that mortgage loans can be provided.

2. A double interest rate system should be implemented so that the interest rate of loans flowing into productive, employment and export sectors is cheaper than the interest rate of loans flowing into the commercial sector. It seems that such an arrangement will encourage active industrialists/businessmen in the productive sector, speed up economic activities, increase productivity and provide great support in import substitution and export promotion, and will also have a positive effect on the development of entrepreneurship and creation of employment opportunities. Similarly, for the purpose of calculating the Capital Adequacy Ratio in the case of non-production loans, the specified risk weight should be reduced by 50%. Such an arrangement seems to be of great help in extending credit to the productive sector and making the economy sustainable.

3. In the current situation, it would be reasonable to reduce the current bank rate of 7.5% by 1% to reduce the pressure on the interest rate. This will help to reduce the pressure on Nepal Rastra Bank and banks and financial institutions and to stop all-round attacks.

4. In view of the contraction in the business of banks and financial institutions, it seems appropriate to postpone the arrangement of Counter Cyclic Buffer of 0.5% which will be implemented at the end of Samvat 2081.

5. A provision should be implemented that the deposit of a period shorter than 1 year cannot be counted in the term. The provision of making short-term term deposits has a direct impact on the expansion of long-term loans as savings deposits are converted into term deposits.

6. Cash Reserve Ratio should be replaced by Net Liquidity Ratio and more flexibility should be provided to banks and financial institutions.

7. The Low Value individual criteria to be calculated for Regulatory Retail Portfolio is Rs. From 1 crore to Rs 2 crore should be raised.

8. In order to achieve the target of 11.5 percent in credit expansion, it would be appropriate to maintain more flexible arrangements in terms of capital adequacy, risk bearing and sectoral limits.

9. Arrangements should be made to provide re-loan facilities for providing cheap loans targeting production-oriented/employment-oriented/export-oriented industries and hospitality sector.

10. For good loans, the loan loss provision should be maintained at only 1 percent.

11. In the current situation of unexpected increase in bad loans of banks and financial institutions, the provision that NPA should not exceed 5% when taking deposits from Nepal Rastra Bank should be removed.

12. In the recovery process of bad loans, the bank should make provision for Capital Gain Tax to be levied only in the case of sale and not when the collateral is sold to the NBA.

13. A clear provision should be made that the non-banking property that is registered in the name of banks and financial institutions cannot be returned to a third person after completing the entire process in accordance with the prevailing law.

14. When the non-banking property registered in the name of a bank and financial institution is transferred to the name of a third person after completing the entire process in accordance with the prevailing law, in the event that the relevant land office raises the issue of land limitation and does not transfer the name, an initiative should be taken through Nepal Rastra Bank for a clear provision that land limitation does not apply in the case of banks and financial institutions.

15. The responsibility of determining the limit of current capital loans should be given to banks and financial institutions. In the same way, although the current capital loan guidelines are very important, the country's environment, needs, time-relevance and possible impact should be discussed among the stakeholders and immediate steps should be taken to improve the currently irrelevant arrangements.

16. The provision made regarding blacklisting of the guarantor should be withdrawn immediately as it is in conflict with the laws and regulations mentioned in the list.

17. At present, the system of showing interest income on accrual basis and paying tax on that basis should be amended and provision should be made to show interest income only in the accrual basis.

Related post

- Digital ICT Media PVT LTD (A Women Group)

- Tarkeshwor, Kathmandu, Nepal

- digitalictmedia@gmail.com

© 2026 All right Reversed.Banks Nepal Pvt Ltd